With the FIFA World Cup recently coming to Canada, reporting entities must take extra measures to help detect and deter potential money laundering offences tied to human trafficking.

Published June 2026 | Regarding FINTRAC Special Bulletin Reference: FINTRAC-2026-SB003

FINTRAC has recently issued a targeted Special Bulletin on human trafficking risks tied to major international sporting and entertainment events. Apt timing given the 2026 FIFA World Cup arriving in Canada this month.

That means for you, a reporting entity with FINTRAC compliance obligations, this bulletin is not optional reading — it has direct implications for your risk assessments, transaction monitoring, and suspicious transaction report obligations during this time and in the future. Especially if you are a MSB, PSP or Financial Institution.

Today our anti-money laundering experts are here to break down what the bulletin says, which human trafficking AML indicators matter most, which sectors are affected the most and what your organization needs to take action on.

And for those of you strapped for time, here is the TLDR; human trafficking and forced labour is always a concern, but its increased prevalence during major international entertainment and sporting events such as the world cup, should remind you to take extra caution. Reporting entities like MSBs, Credit Unions and Financial Institutions should be extra vigilant for indicators of human trafficking and forced labour during the world cup.

What Is FINTRAC Special Bulletin FINTRAC-2026-SB003?

Issued in May 2026 under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, this Special Bulletin provides guidance on financial transactions associated with the laundering of proceeds from human trafficking connected to major international events — including the FIFA World Cup. The bulletin covers two distinct trafficking types: sexual exploitation and forced labour.

The bulletin is directed at all reporting entities subject to the Act, especially banks, credit unions, money services businesses (MSBs), virtual asset service providers, and payment processors registered as MSBs. Its indicators are designed to support suspicious transaction report (STR) filings where human trafficking proceeds are suspected.

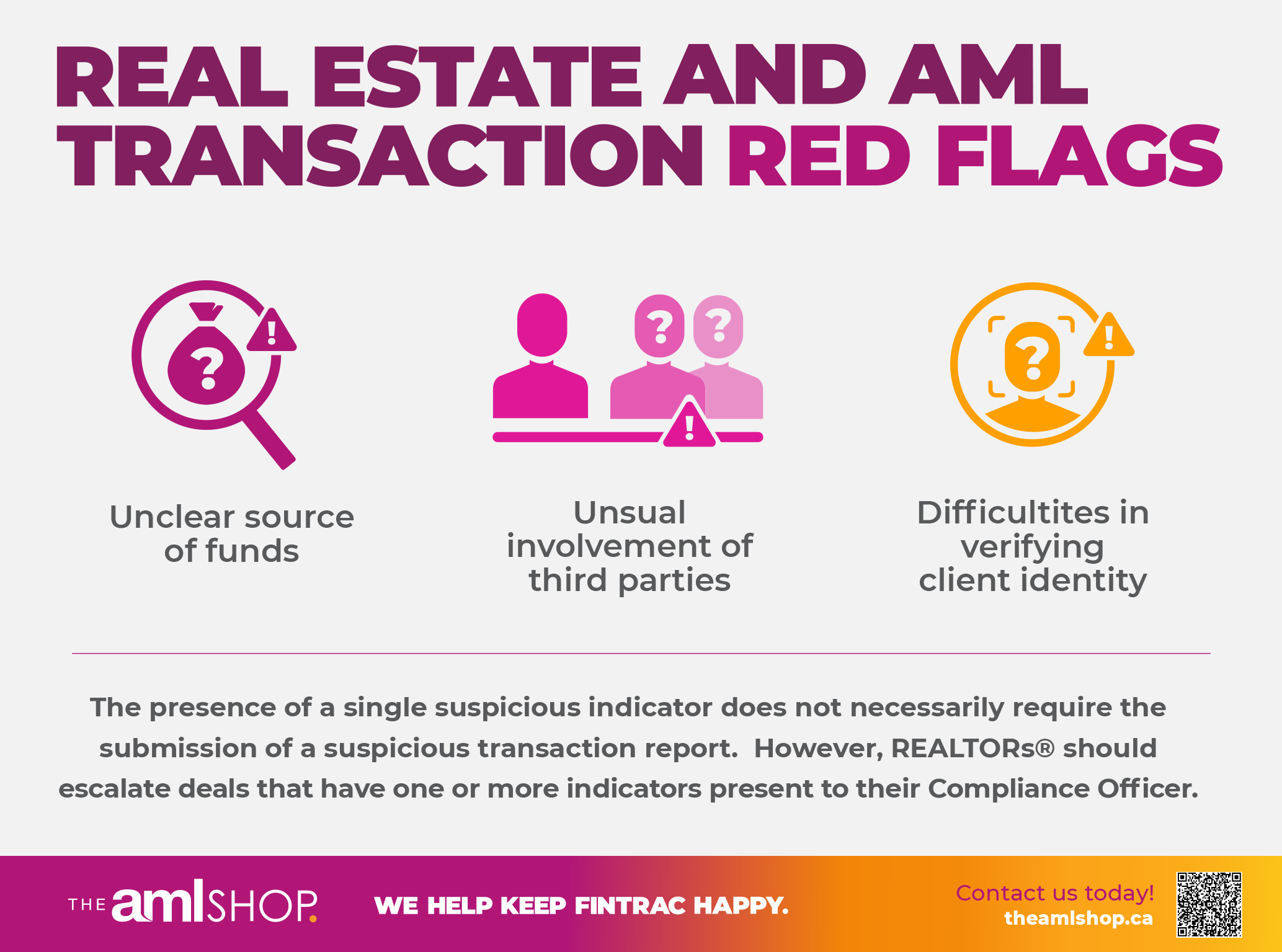

Events Amplify Existing Trafficking Networks - Your RBA Matters here.

One of the most important insights in this bulletin — and one that should directly shape how your compliance team frames its Risk Based Approach (RBA) — is that AML compliance connected to large sporting and entertainment concerns are not about new criminal actors arriving for the event. For more information on your RBA and why it matters in the context of Canada’s overall risk framework, read our 2025 National Risk Assessment update.

Human trafficking linked to major events primarily involves existing domestic networks that scale up activity, reposition victims, or shift operations toward areas of concentrated demand.

The event acts as a catalyst to amplify, not an origin point.

For compliance purposes, this means the human trafficking AML indicators to watch for are extensions of known typologies, calibrated for the specific conditions large-scale events create: compressed timeframes, geographically concentrated activity, elevated cash usage, and heavy reliance on informal or subcontracted labour arrangements.

The following indicators are drawn from FINTRAC Special Bulletin FINTRAC-2026-SB003 (May 2026) https://fintrac-canafe.canada.ca/intel/bulletins/sport-eng

💡 Pro-tip In our view, the below indicators do not need to be read as a checklist, but are most powerful when taken into consideration against what your team already knows about a client’s typical behaviour and their risk profile.

Human Trafficking AML Indicator #1:

Sexual Exploitation

Major influxes of short-term visitors drive concentrated demand for commercial sexual services near event venues, hotels, entertainment districts, and transportation hubs. Traffickers coordinate primarily through online platforms — escort sites, classified ad platforms, and encrypted messaging apps — with financial activity following quickly behind.

PSPs, MSBs and Financial Institutions are going to face the most vulnerabilities here.

AML Indicators Associated With Perpetrators

The following human trafficking AML indicators are flagged by FINTRAC for reporting entities assessing potential facilitators of sexual exploitation:

Accounts receiving unusual spikes in peer-to-peer payments from multiple unrelated individuals during the event period

Incoming funds rapidly withdrawn, transferred onward, or redistributed with minimal balance retention and little evidence of personal spending

Payments for online escort advertising, premium listings, or advertising credits made on behalf of multiple individuals by a single account holder

Clusters of hotel or short-term rental expenses coinciding with frequent late-night or early-morning ATM withdrawals

Frequent transfers to virtual currency exchangers following peer-to-peer deposits associated with escort activity

Multiple accounts linked through shared contact details, devices, or overlapping transaction timing, suggesting centralized financial control

AML Indicators Associated With Demand

These indicators may point to clients purchasing commercial sexual services during the event:

Repetitive low-to-mid value peer-to-peer payments to multiple recipients within condensed timeframes

First-time electronic transfers to previously unknown recipients shortly before or during the event

Payment descriptions containing terminology associated with escort services, aliases, or coded language

ATM use in or near hotels or short-term rental properties following peer-to-peer payments

AML Indicators Associated With Victims

Accounts belonging to victims of sexual exploitation may show:

Incoming funds rapidly transferred onward, consolidated, or withdrawn by a third party

Multiple clients exhibiting similar transaction patterns, shared identifiers, or overlapping payment timing

Accounts that receive frequent deposits but remain consistently depleted with no discretionary spending

A third party appearing to direct or control account activity

Human Trafficking AML Indicator #2:

Labour Trafficking

Events of this scale generate enormous short-term demand for labour in hospitality, cleaning, security, construction, transportation, and food services. Tight timelines and heavy subcontracting reduce oversight and allow exploitation to embed within otherwise legitimate-looking business arrangements — making MSB compliance and banking sector vigilance especially important.

AML Indicators Associated With Perpetrators

Businesses in event-related sectors showing suppressed, irregular, or absent payroll activity relative to apparent workforce size

Multiple workers' wages deposited into or controlled by a single account holder

Frequent transfers between business and personal accounts with circular movements or vague payment descriptions

Cash deposits or electronic transfers clustered around known worksites or temporary worker housing

Payroll accompanied by recurring transfers described as fees, rent, travel, or recruitment costs that appear disproportionate to earnings

AML Indicators Associated With Victims

Payroll received in round-dollar amounts and withdrawn the same day or within a short window, depleting the account to near zero

Minimal or no spending on basic living needs despite evidence the client is working during the event period

Transaction descriptions referencing immigration or recruitment fees — LMIA, work permit, recruitment costs — appearing to be borne by the worker, not the employer

A client who appears accompanied, monitored, or directed by a third party when conducting transactions

Open-source checks revealing a single address associated with an unusually large number of workers, accounts, or businesses

Which Reporting Entities Are Most Exposed?

Large Sporting and entertainment event AML compliance obligations apply across the reporting entity spectrum, but some sectors carry heightened exposure:

Banks and credit unions have the broadest visibility — into peer-to-peer payment patterns, ATM behaviour, accommodation spending, and payroll activity. Front-line staff and transaction monitoring systems need to be calibrated for event-period surges in these patterns.

Money services businesses (MSBs) face elevated risk through cash transactions, prepaid instruments, and transfers to virtual currency exchangers. MSB compliance teams should ensure their monitoring systems account for the geographic concentration of suspicious activity around event venues and host-city entertainment districts.

Virtual asset service providers are specifically flagged in relation to sexual exploitation proceeds moving through crypto following escort-related peer-to-peer activity.

Payment processors registered as MSBs — including payment gateways — also fall within scope. While a hotel or booking platform is not itself a reporting entity, the payment infrastructure beneath it may be. A gateway processing payments for accommodation or advertising services may have visibility into suspicious patterns: a single account paying for multiple short-term bookings across different individuals, or recurring payments to escort advertising platforms.

Suspicious Transaction Report Requirements: What You Must Do

Where there are reasonable grounds to suspect a financial transaction is related to the laundering of human trafficking proceeds, a suspicious transaction report must be submitted to FINTRAC as soon as practicable. The standard is reasonable grounds to suspect — not proof. If you are uncertain, the obligation defaults toward reporting.

FINTRAC has made a specific operational request: include #ProjectPROTECT or #PROTECT in Part G (Description of Suspicious Activity) of any STR related to suspected human trafficking. This tag allows FINTRAC to route intelligence efficiently to its law enforcement partners.

Practical Compliance Steps for Reporting Entities

1. Update your company-wide risk assessment or Risk Based Approach (RBA). If your current assessment predates this bulletin, it should be revisited to reflect the heightened risk environment created by the FIFA World Cup and similar large-scale events.

2. Refresh staff training on event-specific indicators. This bulletin contains targeted financial patterns — not general human trafficking awareness content. Front-line staff handling onboarding, transaction review, and alert investigation need to be familiar with the specific indicators outlined above.

3. Calibrate your transaction monitoring systems. Ensure your systems are tuned to detect peer-to-peer payment spikes, same-day payroll depletion, accommodation-linked ATM clustering, and other event-period patterns described in the bulletin.

4. Review your STR tagging procedures. Confirm that staff filing STRs related to human trafficking know to include the #Project PROTECT tag in Part G.

5. Consult FINTRAC's supplementary resources. The bulletin cross-references FINTRAC's 2021 Operational Alert on laundering proceeds from human trafficking for sexual exploitation, which provides additional indicator detail. The Financial Action Task Force (FATF) has also published relevant typologies on financial flows from human trafficking.

Now, the above steps are not just simple executions - as we have mentioned several times in this piece, knowing exact risks profiles based on your industry, client base and their geographical nuance requires an expert lens.

Our experts at The AML Shop have navigated thousands of engagements from every reporting sector - we know how to translate bulletins like this into a compliance program that holds up under scrutiny .

Frequently Asked Questions

Does this bulletin apply to concerts and entertainment events, not just sports? Yes. The bulletin explicitly covers "major international sporting and entertainment events." Any large-scale event generating significant visitor influxes, concentrated hospitality demand, and short-term labour needs falls within the spirit of this guidance.

What is the threshold for filing a suspicious transaction report related to human trafficking? Reasonable grounds to suspect — not certainty, and not proof. If transaction patterns align with the indicators in this bulletin alongside other contextual factors, that may be sufficient grounds to file.

Are hotels and booking platforms reporting entities under the Act? No. However, payment processors and gateways that are registered MSBs are reporting entities and may have visibility into suspicious payment patterns associated with accommodation bookings or escort advertising.

Where do I send questions to FINTRAC about this bulletin? Email guidelines-lignesdirectrices@fintrac-canafe.gc.ca with Special Bulletin FINTRAC-2026-SB003 in the subject line, or call 1-866-346-8722.

Summary

FINTRAC's May 2026 Special Bulletin is a significant FINTRAC compliance update for any reporting entity operating in Canada. Large scale international sporting events and entertainment creates conditions that existing trafficking networks will exploit — and Canada's regulated financial sector is the first line of defence.

Understanding the human trafficking AML indicators in this bulletin, calibrating your systems, and filing timely suspicious transaction reports with the correct #ProjectPROTECT tag are the minimum steps your organization should take now.

Contact Us for more information on this new development and your obligations (button to contact).

We Help Keep FINTRAC Happy .

This post is for informational purposes only and does not constitute legal advice. For full obligations under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, refer to the Act and associated Regulations directly. This content is not affiliated with, endorsed by, or associated with FIFA or the FIFA World Cup.