The FATF Plenary was recently held in Paris and Canada’s 2026 FATF mutual evaluation was conducted; its first evaluation since 2016. Most regulated entities and compliance officers are aware that the FATF Canada evaluation happened but few can explain what the FATF mutual evaluation is, what assessors actually test or why the verdict affects their go forward compliance and examination exposure with regulators, including FINTRAC.

We expect the mutual evaluation report to land within 1-4 months. At this point, get ready - compliance officers can expect impactful updates to the Proceeds of Crime (Money Laundering) and Terrorist Financing (PCMLTFA) and other legislation.

In this expert article our team brings to you all the details you need to know about the evaluation timeline and why this matters for your program.

What FATF is and what a mutual evaluation assesses

The Financial Action Task Force (FATF) is an inter-governmental body that sets the global standards for combating money laundering, terrorist financing, and proliferation financing. Its 40 Recommendations are the baseline against which every member country's AML regime is measured.

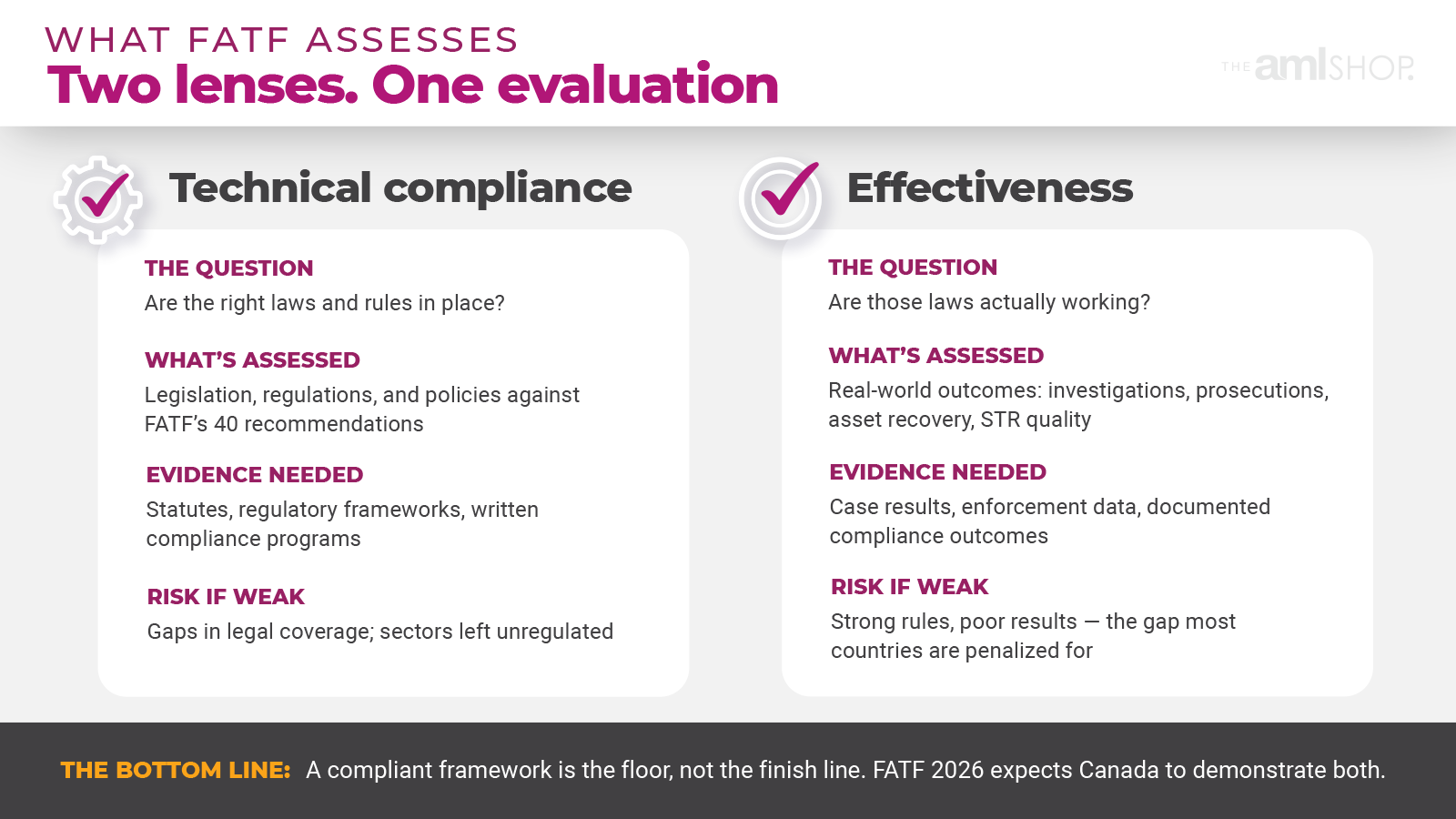

FATF periodically conducts a mutual evaluation of each member country, assessing two dimensions: technical compliance (where laws and regulations are tested and meeting the 40 requirements) and effectiveness (are these laws actually producing results that mitigate ML/TF risk?).

The 2026 fifth-round evaluation will, to no surprise, weigh effectiveness more heavily than previous rounds. Similar to what we have seen in regulatory updates in Canada (see Bill C-12) having a paper document with your compliance policies just won’t cut it any longer - it must be proven effective in practice and the FATF will examine how successful Canada has been at implementing policies to uphold this mandate. For example, the FATF wants to see that STRs lead to investigations, that risk-based monitoring identifies anomalies, and that supervision produces enforcement outcomes.

The outcome of a FATF mutual evaluation in any national context, including Canada, sets the stage for future regulatory updates or changes.

Canada’s last FATF mutual evaluation in 2016 found substantial gaps in critical areas like beneficial ownership transparency, real estate oversight (a high risk sector) and total money laundering prosecution rates. To address these deficiencies, since 2016 Canada has worked to improve. This is evidenced in:

The Federal Beneficial Ownership Registry (launched 2024)

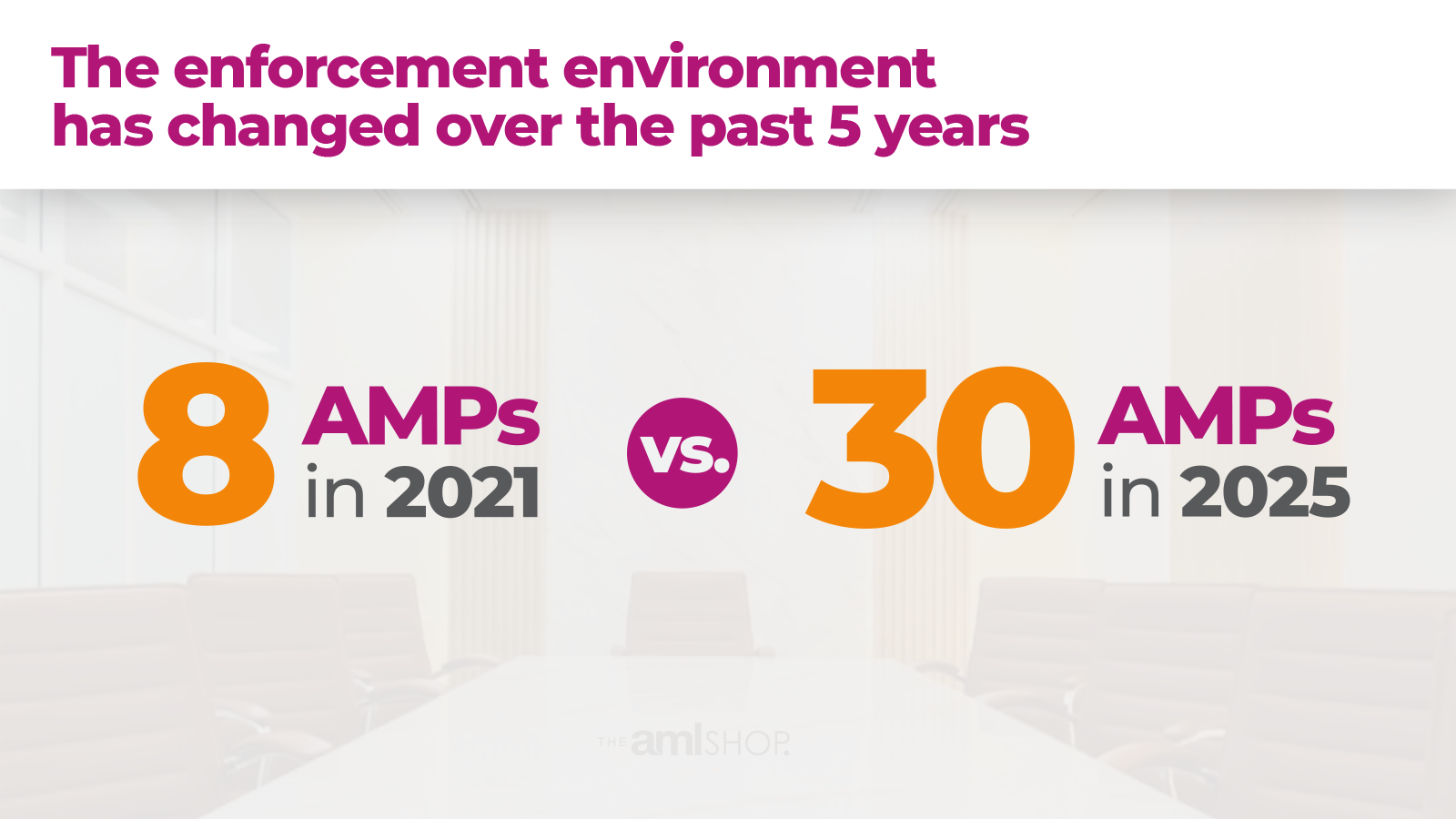

Bill C-12 (although newer legislation without proven results yet, the codifying of the effectiveness standard and increasing Administrative Monetary Penalties by 40x shows a move forward to increased enforcement and heightened consequences as already evidenced in the recent $177M fine to FMSB, Cryptomus)

Expansion of regulated sectors (Finance, Leasing, Factoring and Cheque Cashers are all newly regulated under the PCMLTFA)

In 2026, the FATF mutual evaluation results will tell us whether this decade of reform has helped close these gaps.

The fifth-round methodology: what assessors actually test

Assessors do not just review legislation; they conduct interviews with FINTRAC, OSFI, law enforcement, reporting entities across sectors, and industry bodies. They look for evidence that the system produces outcomes, not just compliance. The core question is whether a nation’s AML regime is preventing, detecting, and disrupting financial crime in practice. Fifth-round evaluations, although following the same process, introduce a more rigorous effectiveness assessment framework.

What is the FATF Methodology?

Effectiveness in a mutual evaluation is assessed across 11 Immediate outcomes rated on a four-level scale from low to high, covering areas including:

The quality of financial intelligence produced by FIUs and whether that intelligence is used in investigations

Whether Money Laundering prosecutions actually produce convictions

The effectiveness of supervision on reporting entities (for example, FINTRAC’s effectiveness in executing on its mandate)

If preventive measures are operating as intended (i.e. Customer Due Diligence, STRs and record keeping)

For Canadian compliance officers thinking about the FATF 2026 Mutual Evaluation, the critical point is this: FATF does not audit your programme directly. But if, for example, FATF rates Canada's supervision of a particular sector as only partially effective, authorities could view that finding as a call to action to intensify examination activity in that sector. Thus, reporting entities would feel the trickle down effect of compliance and examination pressure.

Why the June FATF Canada 2026 verdict matters to your compliance program

FATF findings become FINTRAC and other regulators’ priorities; this is why the June 2026 verdict matters.

As evidenced in post-2016 FATF mutual evaluation when real estate and beneficial ownership were identified as weak spots - FINTRAC increased examination intensity in this sector significantly (in fact, Real Estate is one of Canada’s most examined and penalized sectors by FINTRAC, with over 25 penalties issued since 2021).

The 2026 results will produce a new set of findings that shape the next cycle - whatever the designation is, every category the FATF flags is a category that regulators will prioritize.

In the FATF Canada Mutual evaluation 2026, three broad outcomes are possible:

Grey-List Status - This is the worst case scenario for Canada as it would spotlight the nation’s deficiencies at a global level, inciting potential trade and economic impact. Under this outcome, Canada would commit to an action plan to remediate its deficiencies under FATF oversight. Foreign Banks would increase due diligence on Canadian Institutions. At a national level, FINTRAC would accelerate enforcement across all sectors.

Enhanced Follow Up - Specific areas of deficiency are flagged as requiring improvement, with obligatory progress reports required at each FATF Plenary. FINTRAC would focus enforcement on the specific categories as outlined by the FATF report.

Regular Follow Up - Best case scenario - Canada meets most requirements with standard FATF reporting.

When the FATF Canada 2026 report drops, expect further regulatory changes to be introduced. Regardless of designation, the program standard will change and evolve. And whatever the report findings illustrate will be the impetus to what changes are introduced, their urgency and how much work they will take to achieve.

What to do with this information before and after the verdict

Before the verdict:

If you have not yet reviewed your program against the latest regulatory changes, including Bill-C12’s effectiveness standard, now is the time. If you haven’t had a good look at where you stand, you can’t benchmark against the changes. Ensure you run a gap review against Canada’s AML Regime, not just against FATF standards- to get an accurate picture, you need to gap against where expectations currently sit in a national context. And despite Effectiveness being the “hot topic” right now - don’t focus only on this aspect. You want to keep in mind categories FATF has historically flagged for Canada, including Beneficial Ownership, Due Diligence, Real Estate Controls, STR quality and record keeping completeness.

After the verdict:

Check fatf-gafi.org/en/the-fatf/outcomes-of-meetings.html for the published outcomes.

We suspect Canada’s FATF Mutual Evaluation 2026 report will be released 1-4 months after the Plenary. Identify which Immediate Outcomes FATF rated as partially or minimally effective for Canada. Each one is a FINTRAC examination priority for 2026 to 2027.

If your firm is in need of a Gap Analysis or compliance advisory, contact our experts today. We can help review your program, monitor your results against the current standard and work with you to update when regulations change, post-verdict.

We Help Keep FINTRAC Happy.

FAQs

-

A FATF mutual evaluation is a peer review process that examines how well a country is protecting its financial system from money laundering, terrorist financing, and proliferation financing. Conducted by the Financial Action Task Force — the global standard-setting body for AML/CTF — these evaluations assess both whether the right laws exist and whether they are actually working. For a country like Canada, a FATF mutual evaluation carries real consequences: findings shape regulatory priorities, influence how international partners view the financial system, and can affect market access.

-

The FATF mutual evaluation of Canada examines the country's full anti-money laundering and counter-terrorist financing regime. For FATF Canada 2026, assessors are focused less on whether legislation exists and more on whether it produces results — are financial crimes being detected, investigated, and prosecuted? Key areas under the microscope include beneficial ownership transparency, suspicious transaction reporting, asset recovery, and coverage of higher-risk sectors like real estate, crypto, and money services businesses.

-

The FATF Canada 2026 evaluation has had a direct impact on FINTRAC enforcement in Canada. In the lead-up to the on-site assessment, FINTRAC significantly increased both the frequency and size of Administrative Monetary Penalties, introduced a tougher supervisory framework, and stopped pre-sharing examination findings with reporting entities before violations are finalized. Legislative changes have also dramatically raised penalty ceilings. The message is clear: Canada is demonstrating to FATF assessors that its enforcement regime has teeth.

-

Canada's mutual evaluation report was adopted at the FATF Plenary in June 2026 — meaning the findings are finalized. Based on the FATF's standard post-plenary review process, the full report is expected to be published within the next few months, likely before the end of 2026. Compliance professionals should use this window to assess where their programs stand and be ready to respond once the report is public.